Should you buy, hold or sell Polynovo shares?

From time to time we identify a truly special business.

In looking at Polynovo, not only is it rapidly taking market share with healthy margins and a large runway for growth, but its offerings are delivering amazing outcomes for surgeons and patients globally.

The history of Polynovo

Polynovo is an Australian medical device company that was incorporated in 2004.

Since that time, it has improved and augmented ground-breaking technology in the space of synthetic bio-absorbable polymers originally developed by the CSIRO's Biomaterials team.

In our view, anything out of the CSIRO absolutely warrants consideration. Polynovo brings a revolutionary, patented and commercially approved skin re-generation product that is seeing rapid sales growth globally and changing lives.

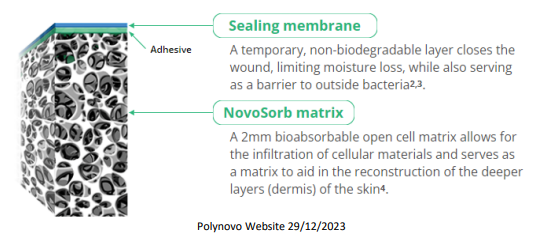

NovoSorb BTM explained

When large wounds and burns occur, there is often significant damage to skin and deeper dermis layers. Essentially, before being able to complete a skin graft, unhealthy/dead skin is removed (or already non-existent) and Novosorb BTM is applied.

This temporarily seals the wound and limits moisture loss via a removable sealing membrane. Essentially, the biodegradable polymer allows cellular migration into the foam-like product, resulting in new blood vessel formation and collagen production throughout the matrix.

This biodegradable product makes a large wound into a series of small interconnected micro-wounds, which significantly increases the chances of re-generation and the area being suitable for skin grafting.

A strong alternative to animal-harvested competitors

The current solutions in the market are primarily produced using animal products such as sheep forestomach tissue, shark cartilage and bovine dermis.

Typically, these products are harder to harvest and if the patient's wound becomes infected, bacteria may infiltrate the animal layer which can be particularly susceptible to infection.

To our understanding, Polynovo's product being a lab-manufactured product, means there are no foreign sensitising proteins or biological material to feed bacterial infection.

In Polynovo's major markets it is a third, to half the cost of its biological competitors, presenting a far more attractive overall value proposition for patients, surgeons and healthcare systems.

First-half results maintain strong momentum

Half-yearly results delivered in February have maintained our confidence, with revenues of $48.8 million increasing by 65.5% against the first-half 2023 financial year figure.

Underlying net profit also increased $5.7 million, from a loss of $2.2 million delivered 12 months earlier. Worth noting is the significant growth in employees, with headcount increasing from 173 to 237, including a heavy focus on expanding their salesforce.

While Polynovo has been consistently hitting sales records already, we are mindful that it can take 6-12 months for new salespeople to build their pipeline and actually convert.

This leaves us particularly optimistic of seeing strong results over the next 12 - 24 months as the benefits of investment into additional sales teams continue to flow through.

The business now operates in around 37 countries, with hospital accounts growing from 515 to 861.

While Polynovo's primary focus has been on the high margin US market, the rest of world (ROW) segment grew at an impressive 122.2% to $10 million, bringing additional confidence around Polynovo's ability to expand its footprint globally, even without heavy resource allocation.

Standout growth from the ROW was delivered by ANZ, UK/Ireland and the Middle East, while India, Hong Kong and Canada are also building momentum. Management have also referenced Japan and China as target countries looking ahead.

Largest ever single order going to Ukraine

With the current increased instance of conflict globally, the number of blast wounds and burns in the likes of Ukraine and the Middle East have risen sharply.

After Polynovo originally donated Novosorb BTM in an effort to help victims, global charities and governments are now looking to purchase Novosorb as one avenue of being able to help those injured in conflict zones.

In February, Polynovo confirmed their largest ever single order, with A$1.2 million paid in full for a shipment of BTM to be delivered to the Ukraine.

A recent training session for around 30 Ukrainian surgeons was also held to assist in the rollout. In addition to this, governments globally are also assessing the possibility of stockpiling Novosorb in large quantities to ensure they're prepared for mass treatment required in the event of terrorism, conflict or natural disasters.

CEO Swami Raote driving business expansion with US and India high on the agenda

30-year Johnson and Johnson veteran Swami Raote has now settled into the CEO role and his intimate knowledge of the industry and strong business networks appear to be a great fit for Polynovo.

The current focus is on the high margin US market, with significant sales force expansion expected to deliver strong growth as traction continues to build, while also targeting the lower margin but extremely large Indian market where we can ideally see the business win large public health tenders.

While they mightn't see the same high margins, the number of trauma and burns in India should provide a large market opportunity, while also helping to deliver positive outcomes for patients in need.

Just this month traction has been made, with an announcement that the Indian government have accepted Novosorb BTM onto the Government-e-Marketplace, the centralised procurement platform for government hospitals throughout India.

Share price momentum continues after October low

While the share price has bounced strongly off 12-month lows around $1.095 in October, the current price still presents a healthy discount to our 12-month price target of $2.80 and all-time high of $4.01 reached in 2020.

There has been capital raised and that does bring some share price dilution, but since that all-time high of $4.01 the business in our view has progressed significantly and is now in far better shape in relation to all key metrics, yet shares can still be brought significantly lower and on a far more palatable revenue multiple.

Not only does Polynovo appear to provide a superior offering in relation to both patient outcomes and costs, but new product development, product improvement, facility expansion and a rapidly growing salesforce leave us optimistic about seeing strong growth over the years ahead.

Get stories like this in our newsletters.