Super's double-digit returns: how long will they last?

Superannuation fund returns continued their eight-year bull run in April, boosted by international shares and a fall in the Australian dollar.

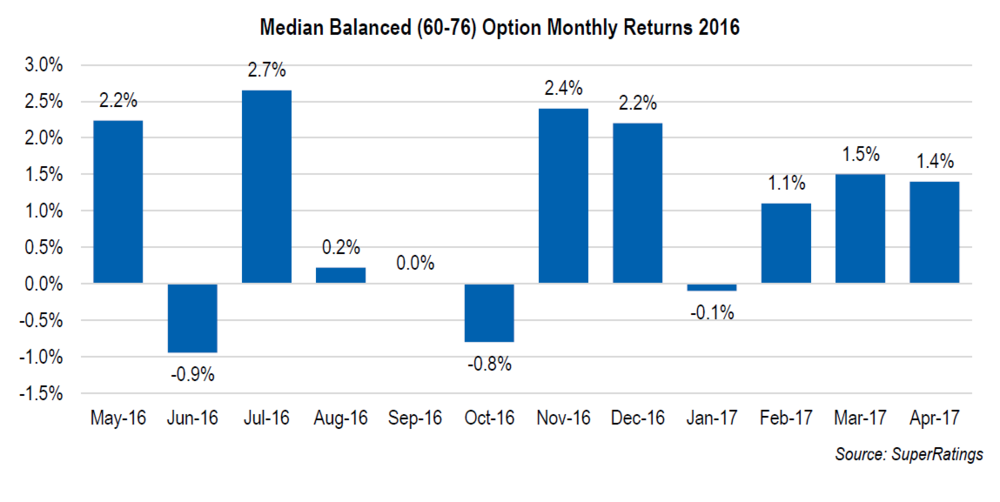

The median balanced option return posted 1.4%, building on the 1.5% returned in March and bringing the financial year to date return to 10.0%.

Even a 300 point loss on Wall St in mid-May wasn't enough to stop the momentum with May now also looking like delivering positive returns for funds.

In Australia, markets have been supported by fundamentals, with full-time employment continuing to grow in April, and manufacturing firmly in expansion. However, there is also evidence of a loss of upward price pressure, partly as a result of declining energy prices and tumbling iron ore values through March and April.

The 2017-18 Federal Budget, delivered earlier this month, presented an optimistic view of the economy, with the path back to surplus in 2020-21 predicated on a gradual lift in wages growth from 1.9% to 3.75%.

"Economic indicators remain robust, although weaker inflation figures may be of some concern to investors as well as central banks," says SuperRatings chairman Jeff Bresnahan.

"We have not seen the strong boost in confidence many have been hoping for, but neither have we seen any sign of a sustained pullback or dramatic loss of momentum.

"Despite the fact that significant risks remain, including in the housing market, the outlook for 2017 remains somewhat positive."

Cash and fixed interest returns remain meagre, sitting at 1.4% and 1.3% for the financial year to date respectively. Australian and global shares have been the star performers for the financial year thus far with returns of 15.3% and 15.6% respectively.

"It would be a great result to achieve a double-digit return for the financial year, but we still have a bit longer to go," Bresnahan says.

"Volatility has begun to increase in line with continued political uncertainty globally, and market momentum is positive. However, investors should be careful not to under-price risk in this environment. In other words, we should not get too complacent."

Global shares rally, but how high is too high?

The Australian market had a mixed month in April, posting a return of 1.0%, weighed down by negative performance from the Materials (-0.2%) and Energy (-0.6%) sectors, and a challenging month for Consumer Staples (-2.6%).

The main gains came from the Industrials sector (+4.4%), with strong gains from Brambles (+10.6%) following its announcement that it is on track to meet its 5% sales growth target. Another recovery story came from the much-maligned Bellamy's, which gained strongly late in the month to post a return of 22.4% with the installation of new management, as well as continued demand for Australian baby formula from the Chinese market.

The US market rally continued unabated through April, with the Dow Jones Industrial Average price index posting a rise of 3.6% - this despite a disappointing GDP reading of only 0.7% for Q1 2017. The French CAC 40 returned 7.1% in April as Emmanuel Macron sailed to victory in the French presidential election, while the EuroStoxx 600 Index gained 5.8%, as confidence in the European recovery continued to build.

"Interestingly, equity market gains have coincided with a fall in yields in major markets, as well as a fall in the US dollar," says Bresnahan.

"With valuations starting to look high in the US, investors are holding out for the President's proposed tax cuts to be made law, which are needed to consummate the reflation trade."

Global yields fell in April, continuing a downward trend started in the previous month. While rates have been trending higher since October 2016 and yield curves have steepened, investors have appeared to embrace duration again, reflected in longer-term fund flow.

The US 10-year Treasury yield fell from 2.39% to 2.28% after reaching an intra-month low of 2.17%. While recent CPI releases in both Europe and the US have been promising, the numbers have moderated in recent months, and core inflation remains below central bank targets.

The inflation question

Longer-term returns for super continue to sit close to funds' inflation targets, with the seven-year return sitting at an estimated 7.8%pa (above most funds' CPI targets).

The 10-year return moved lower to 4.8%pa, although it remains impacted by the Global Financial Crisis, which occurred nearly 10 years ago.

The point of maximum monetary stimulus has passed, signalled by the US Fed's March rate hike, although monetary policy remains very accommodative globally, and quantitative easing measures in Europe have not yet been tapered.

Compared to a year ago, when the FYTD return was 1.4%, there has been a strong turnaround in returns, but the idea of returns being lower for longer is still a key point of discussion in the industry.

While inflation appears to be taking hold, it has moderated in recent months, prompting central banks, and especially the US Fed, to reconsider the pace of tightening.

Get stories like this in our newsletters.