Why smashed avocado isn't the problem with housing affordability

There's always been plenty of debate about why younger people can't enter the housing market, and in recent weeks it has kicked up a gear.

The suggestion is that if young people stopped drinking coffee or stopped purchasing smashed avocado on toast they would be able to afford to buy.

My view is that this smashed avocado problem is a great generalisation; the reality, as is often the case, is that it is not so simple.

While the value of properties continues to rise across most of the country (not so in Western Australia and Northern Territory), wages and household income growth are at historically low levels.

What this means is that as home values grow, wage growth is not keeping pace and potential first-time buyers are finding it more difficult to save a sufficient deposit to purchase a home.

While lower interest rates make servicing a mortgage easier, low income growth and strong property value growth make saving for the initial deposit much more difficult.

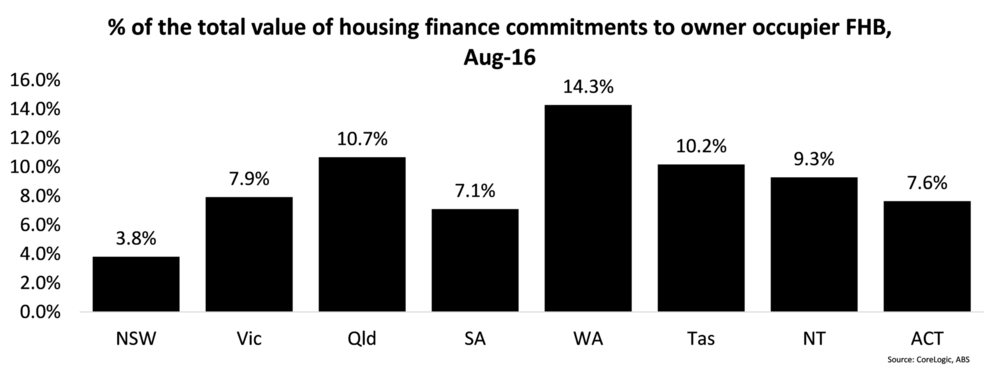

It's always good to look at the data, which shows that the proportion of total mortgage lending going to owner-occupier first-home buyers is somewhat thin.

In each state and territory, less than 15% of the value of all housing finance commitments went to first-home buyers purchasing for owner-occupation in August.

In fact, in all cities the value of lending to investors was substantially higher than it was to owner-occupiers.

Given this, it is no wonder we continually hear anecdotal commentary that an increasing number of people who don't own a home are looking to purchase investment properties and/or choosing to rent.

This is especially evident when you consider the tax deductions that are available to an investor but are not afforded to an owner-occupier.

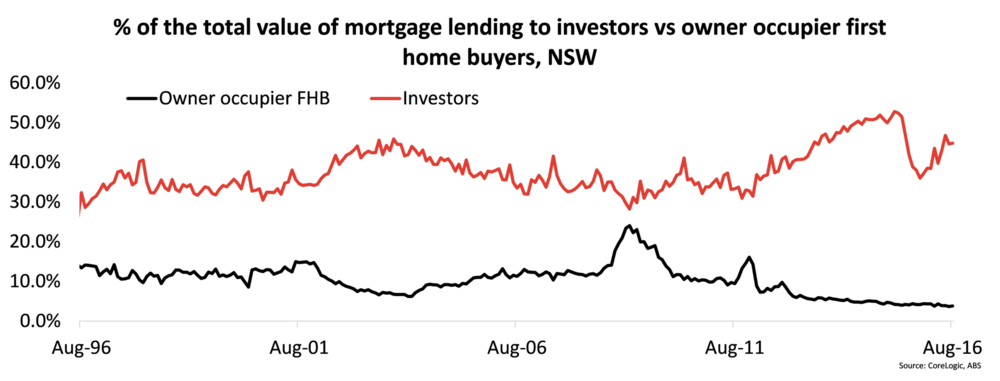

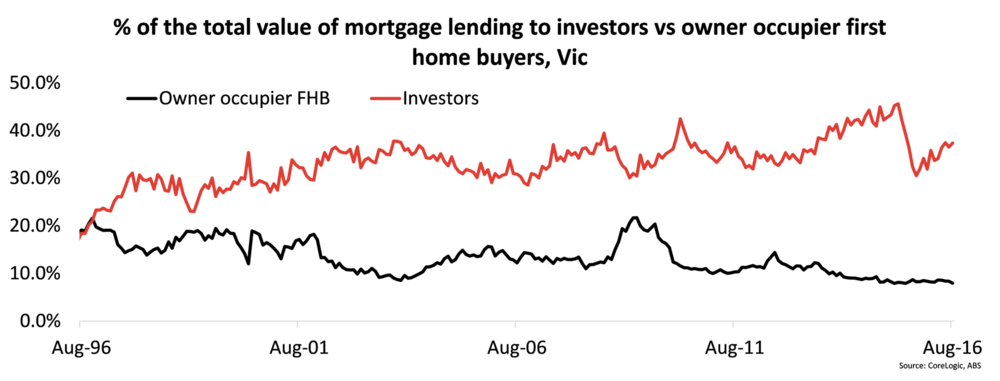

The following two charts show the proportion of total mortgage lending to owner-occupier first-home buyers and to investors over time in NSW and in Victoria.

Evident in the charts is that investors have always been more active in the market than owner-occupier first-home buyers. However, there are a few points to make with this data.

First, it is unclear both now and historically how many investors are first-home buyers, as it is not data that is tracked.

Second, because we don't know the number of investment housing finance commitments, only the value, things become a little unclear especially when you consider that owner-occupier first-home buyers on average have a smaller loan than other owner-occupiers.

Nevertheless, for both states over time there is evidence of heightened investor activity while first-home buyer activity shrank.

With investment activity recently at historic high levels, it is no wonder that first-home buyer activity is at an all-time low.

So all this analysis prompts the question of how governments can get people to purchase their own home.

Clearly, lower interest rates that have led to higher prices have only encouraged a greater level of housing investment at the expense of first-home buyers purchasing for owner-occupation.

Get stories like this in our newsletters.