Five ways to prepare for rising interest rates

With interest rates at half-century lows, we have become accustomed to living in a world where we can borrow money at an interest rate of less than 5%pa.

For the past two and a half decades, central banks around the world have used interest rates as a tool to control inflation. Inflation is when the cost of goods and services we use increase over time.

Around the world, we are now expecting inflation to rise, which means we can expect interest rates to rise. In the March quarter we saw year-end inflation increase to 2.1% up from 1.5% in the December quarter, firmly in the RBA target range of 2% to 3%.

So what does this mean for home owners?

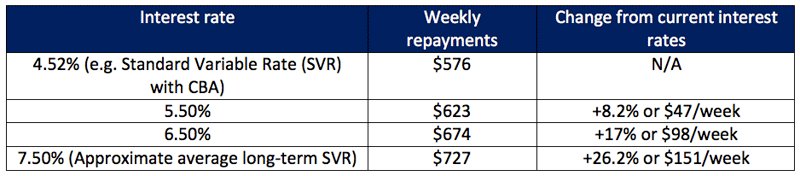

If you have an average home loan of $353,700 and you are making principal and interest repayments the below table shows your weekly loan repayments:

Now let's put this into context.

The average income in Australia is $1533.10 per week or $79,721 each year. The average Australian is saving around 5% of their income or $3986 each year. Assuming a double income household, that makes household savings of just under $8000 a year.

If interest rates increase by 1% in a year loan repayments will increase by $2444 on the average sized loan that is eating away at household savings.

When interest rates increase to an average of 7.50%, repayments will increase by $7852 a year and replace all of household savings.

If you have a home loan you need to start preparing for a world of rising interest rates. Here is what you can do:

- Build a cash buffer

I always recommend that clients have enough for at least six months of expenses put aside as a cash buffer.

This will help to shield you from any immediate increases in interest rates and give you time to adjust any spending commitments. A scary fact that came out from the RBA last week was that one-in-three households only have enough cash on hand to meet one month's mortgage payments.

- Ensure you have an offset account

Offset accounts are a great way to get your surplus cash working for you. Your savings and everyday cash flow will be used to reduce the repayments on your home loan.

For example, if you have $100,000 of loan outstanding and you have $10,000 in the offset account, the bank will only charge you interest on the $90,000 (the value of the loan less what you have in the offset account). This will save you more money than what you can currently make in a high interest cash account.

- Consider fixing interest rates

You can now fix interest rates for a period of up to seven years. I would not recommend fixing all of your loan. A balance needs to be achieved in what you can repay and what you can't repay over the period that you may be fixing some of you loan.

For example, if our family in the above example can save $8000 a year and we want to fix some of their home loan for five years, we would budget that at best they can put $8000 a year into their offset account or $40,000.

The idea would then be to double this amount in the event of any pay increases, bonuses, inheritances etc. They could then ensure they leave around $80,000 as a variable loan. That leaves $273,000 outstanding.

Again, they would not fix all of this straight away but might fix half now and the other half in 6-12 months' time. This helps to average out when the fixed rates expire.

If they were to fix two tranches of $135,000 over the next year at an average fixed rate of 5%pa and variable interest rates were to increase to 7.50%pa within the next five years (a real possibility), weekly repayments would be $630 each week.

This means a saving of $97 a week, or $5000 each year, on mortgage repayments.

- What if you cannot save a cash buffer?

What do you do if you cannot save money at the moment? You are at risk of struggling to make repayments if interest rates start to rise.

Do you have equity in your home? You may be able to apply for a line-of-credit or get a new loan with an offset account to be your cash buffer.

However, you must be disciplined that you do not use this credit facility as a new cash pot to buy a bigger flat screen TV or fund a cheeky trip to Thailand.

This way at least you have some access to cash when interest rates start to rise and you can determine what spending changes you need to make to keep ahead.

- Keep a real budget of household expenditure

The excuse of no longer knowing where you spend your money is lazy.

With automatic budget tracking programs such as Moneysoft or MoneyBrilliant, it is easy to keep tab and properly categorise your expenditure on your credit cards, loans and offset accounts. Knowing where you spend your money will help you to set a realistic budget.

People who track their spending use their hard earned cash a lot more wisely. It will also help you to prepare for where interest rates need to be before your cashflow may get a little tight.

It is a reality that interest rates cannot stay as low as they currently are forever.

Knowing your home loan commitments and paying some attention to your finances will help ensure you are not squeezed by rising interest rates.

Get stories like this in our newsletters.