What the 2015 federal budget will mean for the age pension

The age pension was always a government benefit that was going to be put under pressure, and this year's federal budget proposes just that.

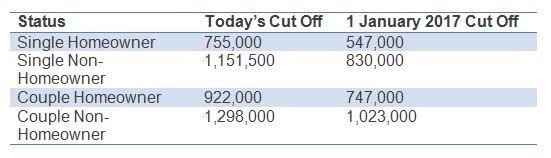

To understand the proposed changes, we need to remind ourselves that to qualify for the age pension you are tested on both income and assets.

Now the good news is that the asset thresholds are increasing.

However, it is on the other side that there is a sting in the tail.

So the first thing we need to do is understand the changes, remembering that the family home is excluded.

There is some relief in that age pensioners who lose their entitlement will be guaranteed eligibility for the commonwealth seniors health card (CSHC) or health care card.

This is an important benefit, providing ongoing access to concessional pharmaceuticals.

However, it is perhaps an unintended consequence that could have the largest impact.

If age pension entitlements are lost altogether, the recipient's superannuation pension will now be income-tested under the more stringent deeming rules that came into force on January 1, 2015.

This makes it even more difficult to access the age pension again in the future, even if assets fall below the cut-off.

For now it is important to future-guard yourself and below are some of my top tips:

- Ensure you have provided to Centrelink the true sale value of your contents. Remember this is not about insurance replacement-value but instead about garage-sale value.

- Although we never like to think of our mortality, funeral bonds and prepaid funerals can receive concessional treatment.

- Your primary home is except from the assets test. It might be worth considering upsizing to a property with greater value. You would, however, need to seriously consider the large transaction costs involved.

- If you are close to the cut-off you may wish to consider gifting assets. This is allowed by Centrelink although there are limits: $10,000 a year, limited to $30,000 over five years.

- If you are looking at moving in with family, perhaps bring forward your move and carefully consider the granny flat exemptions available.

With time on your side, now is the time to get prepared and get advice about how these changes will impact you.

Get stories like this in our newsletters.