The real impact of the property depreciation changes

In an attempt to reduce pressure on housing affordability, the federal government has announced dramatic changes to the way depreciation is claimed on residential investment properties.

Understandably so, we at Washington Brown have been inundated with queries regarding this matter and I will address the main questions. But before I get into the changes, let's start with the basics.

What is property depreciation?

Just as you can claim wear and tear on a car purchased for income-producing purposes, you can also claim the depreciation of your investment property against your taxable income.

There are two types of allowances available: depreciation on plant and equipment, and depreciation on building allowance. Plant and equipment refers to items within the building, such as ovens, dishwashers, carpet and blinds. Building allowance refers to construction costs of the building itself, such as concrete and brickwork. Both of these costs can be offset against your assessable income.

How does a depreciation schedule help me?

Simple. A depreciation schedule will help you pay less tax. The amount the depreciation schedule says you can claim effectively reduces your taxable income.

Depreciation is known as a "non-cash deduction" because it's the only deduction that you don't have to pay for on an ongoing basis. The deductions are built into the purchase price of your property.

All other deductions, such as interest levies, will hurt your hip pocket on an ongoing basis.

What are the changes?

The government will limit plant and equipment depreciation deductions to outlays actually incurred by investors. In essence, unless you as the buyer have physically purchased the items you can no longer depreciate them. This is a massive change to what you can claim and significantly reduces an investor's cash flow.

If I already own an investment property and I'm claiming depreciation, how will it affect me?

The good news is that it won't: any existing investment properties purchased (contract exchange date) before 7.30pm on May 9, 2017, are not affected. Get a quote now to start claiming the plant and equipment depreciation - it could be your last chance!

Will I need a quantity surveyor's report in the future?

Great news: yes, you will. This is because these changes relate only to the plant and equipment of the building and not the capital works deduction (that is, the structure of the building). To put this into perspective, the plant and equipment component typically only represents about 10% of the construction cost of a new build, so there's still 90% of the overall claim left.

If I buy a brand-new property now, do these changes apply to me?

From July 1, 2017, the government will limit plant and equipment depreciation deductions to outlays actually incurred by investors in residential real estate properties. Plant and equipment items are usually mechanical fixtures or those that can be "easily" removed from a property such as dishwashers and ceiling fans.

Here's the uncertainty ... Who actually acquired the plant or equipment? The developer? The builder? The property investor who purchases the new property? We suspect that when the legislation is finalised, you'll still be able to claim depreciation on the plant and equipment if the property is brand-new. This will be a boon for property developers. However, I believe it will make it very hard to sell a near-new property in the future.

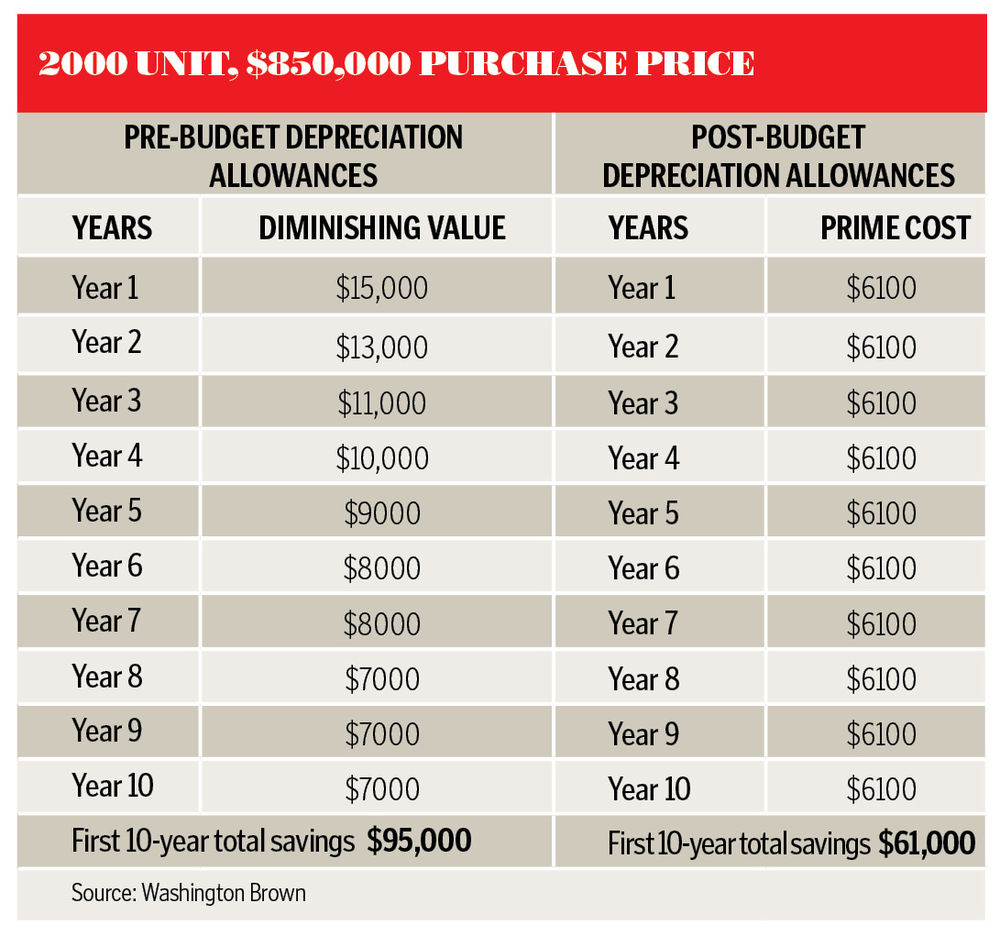

What are the numbers?

This table shows the difference between pre-budget and post-budget depreciation claims for a residential property that was built in 2000 and purchased for $850,000.

The first-year allowance alone changes from around $15,000 down to around $6000.

And the overall difference in deductions over the first 10 years is in excess of $30,000.

The most significant impact is in the early years of the property ownership. This is usually when an investor needs the allowances the most to be able to afford the property.

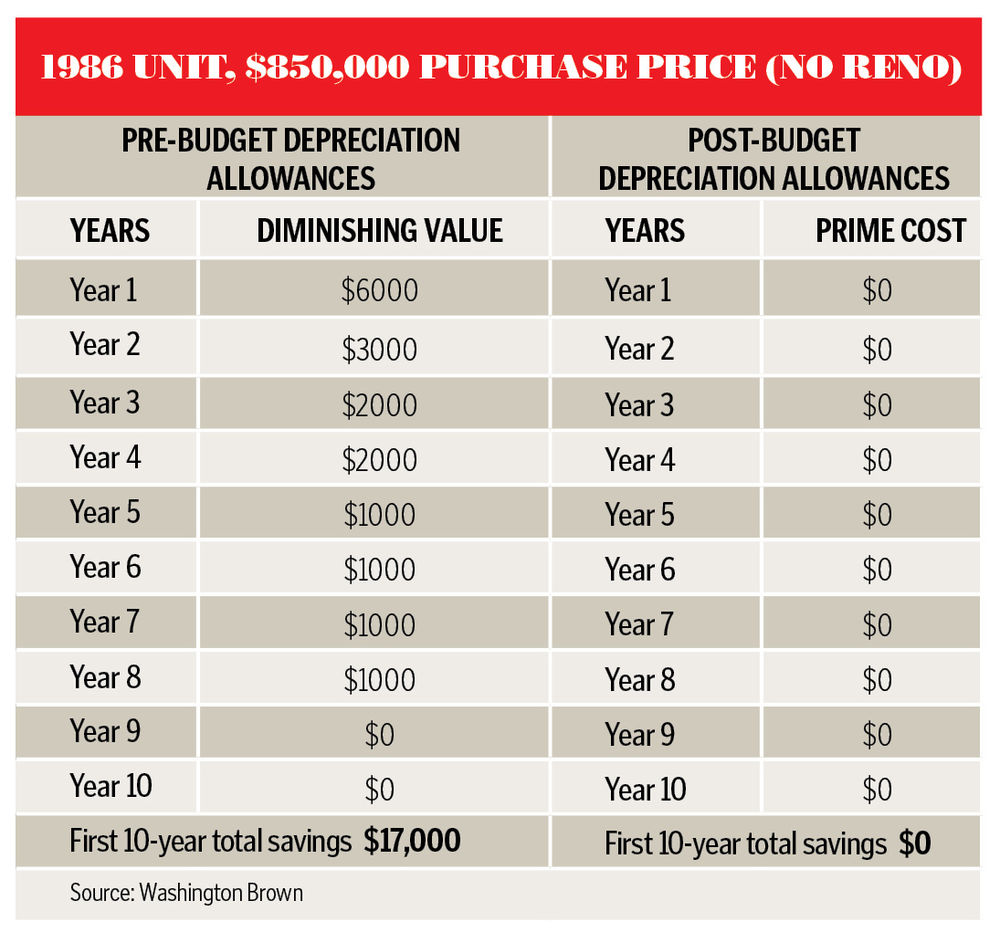

The second table (below) highlights how the proposed changes will affect a property, built in 1986, that has had no renovation.

Previously, when an investor bought this type of old property the first-year deductions were in the order of $6000; now they will be nil.

It's pretty rare for this to occur in reality, as most properties built that long ago have had some form of renovation, making a depreciation schedule still a worthwhile exercise.

What happens to the plant and equipment that I have bought?

Acquisitions of existing plant and equipment will be reflected in the cost base for capital gains tax purposes for subsequent investors. It is unclear at this stage what happens in terms of depreciation to an item that you acquire at settlement, then remove during the ownership of the property.

You are, however, quite entitled to claim depreciation on any item you actually purchase and can claim this over the effective life of that asset while you remain the owner.

Why is the point of it all?

The government is attempting to reduce pressure on housing affordability. Also, according to the budget statement, "this is an integrity measure to address concerns that some plant and equipment items are being depreciated by successive investors in excess of their actual value".

I agree with this statement. There is a problem with the way second-hand plant and equipment items when attached to buildings are being valued at the moment. The current legislation is not clear on how to value these items and as such varying valuation methods are being carried out by practitioners.

Get stories like this in our newsletters.